What Is PMI? A Homebuyer's Guide to Private Mortgage Insurance

Learn what PMI is, when it’s required, how much it costs, and how to avoid or remove it an essential guide for today’s homebuyers.

If you’re planning to buy a home, especially with a conventional loan and less than 20% down, you've probably heard the term PMI tossed around. But what is PMI exactly? And why do lenders require it?

In this guide, we’ll break it down clearly no jargon, no fluff. You’ll learn what PMI is, how much it costs, when it applies, and how to avoid or remove it. Whether you’re a first-time buyer or revisiting the mortgage process, understanding PMI can help you make smarter decisions and potentially save thousands.

What Is PMI?

PMI stands for Private Mortgage Insurance. It’s a type of insurance that protects the lender, not the buyer, in case the borrower stops making mortgage payments (also known as defaulting on the loan).

So why do lenders require PMI? It’s all about risk. When a buyer puts down less than 20% on a home, the loan is considered riskier. PMI is essentially a safety net for lenders in case you walk away from the loan.

In short, PMI allows you to buy a home with less money down but it comes at a cost.

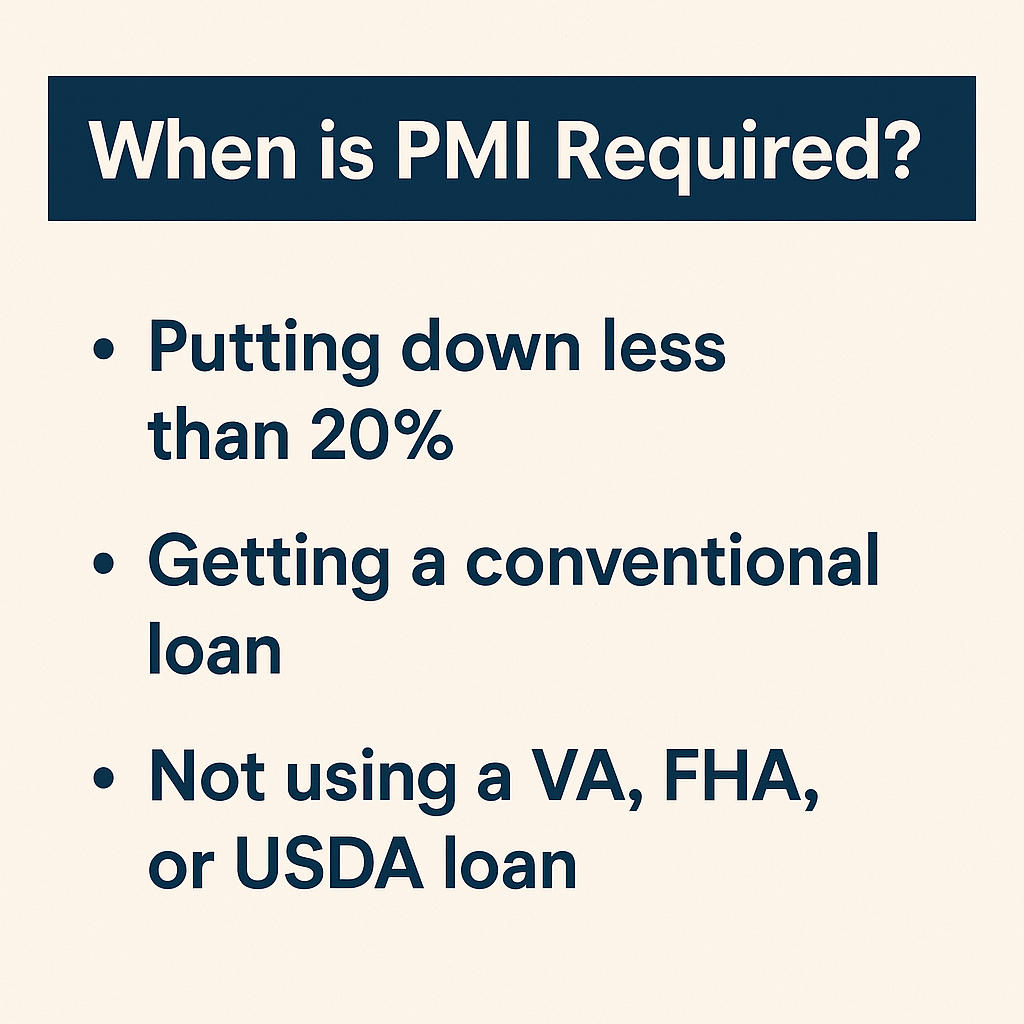

When Is PMI Required?

PMI is typically required on conventional loans when you:

- Put down less than 20%

- Borrow through private lenders (vs. government programs)

- Do not qualify for a VA loan, FHA loan, or USDA loan

Let’s say you want to buy a $400,000 home and only have $40,000 for a down payment (10%). You’ll likely need PMI.

On the other hand, if you’re putting down 20% or more or using a government-backed loan you can avoid PMI altogether.

How Much Does PMI Cost?

PMI rates usually range from 0.3% to 1.5% of your loan amount annually. Several factors influence your specific rate:

- Loan amount

- Credit score

- Down payment size

- Loan type

- Lender and PMI provider

Let’s do some quick math:

| Loan Amount | PMI Rate (Annual) | Estimated Monthly PMI | | --------------- | --------------------- | -------------------------------- | | $300,000 | 0.5% | $1,500 per year / $125 per month | | $400,000 | 1% | $4,000 per year / $333 per month |

The lower your credit score and down payment, the higher your PMI cost tends to be. A buyer with a 760 credit score and 15% down will likely pay less PMI than someone with a 640 credit score and 5% down.

How Do You Pay PMI?

Lenders typically offer four ways to pay PMI:

-

Monthly Premiums: The most common method. PMI is added to your monthly mortgage payment.

-

Upfront Premium: A one-time payment made at closing. You may avoid monthly payments, but it increases your cash needed at the start.

-

Split Premium: A combination of upfront and monthly premiums. This reduces both your closing costs and monthly mortgage burden.

-

Lender-Paid PMI: The lender covers the PMI but charges you a higher interest rate. This can be appealing short-term but may cost more over time.

Always compare options with your lender to understand the long-term financial impact.

Is PMI Tax-Deductible?

As of the most recent tax laws, PMI may be tax-deductible, but only under certain conditions:

- Your income is below the IRS phaseout threshold (usually under $100,000–$110,000 for single filers).

- You itemize deductions instead of taking the standard deduction.

Always consult a tax professional to see if you qualify.

How to Avoid PMI

Avoiding PMI is possible. Here are your main strategies:

1. Make a 20% Down Payment

This is the most straightforward way to bypass PMI. For a $350,000 home, that means $70,000 down. Not everyone has that, but if you do, use it.

2. Use a VA Loan (If Eligible)

VA loans, offered to eligible veterans and active-duty military, don’t require PMI regardless of down payment size.

3. Explore a Piggyback Loan (80-10-10)

In an 80-10-10 loan, you finance:

- 80% with a first mortgage

- 10% with a second mortgage (like a HELOC)

- 10% as your down payment

You avoid PMI, but now you’re managing two loans. This method isn’t right for everyone and may have higher interest rates.

4. Look for Lender-Paid PMI Promotions

Some lenders offer promotions where they cover PMI for you often in exchange for a slightly higher interest rate.

How to Get Rid of PMI

If you already have PMI, don’t worry it won’t last forever.

Here’s How to Remove PMI:

1. Automatic Termination (By Law)

When your mortgage balance hits 78% of the home’s original value, the lender is legally required to cancel PMI assuming you’re current on payments.

2. Request PMI Cancellation at 80%

You can request PMI cancellation once you reach 20% equity based on your original purchase price or appraised value.

You’ll need to:

- Make the request in writing

- Have a good payment history

- Possibly pay for a home appraisal

3. Refinance Your Loan

If your home has significantly appreciated, you can refinance into a new loan without PMI, especially if your new loan-to-value ratio is under 80%.

Pros and Cons of PMI

Pros

✅ Allows you to buy a home with less money down

✅ Lets you enter the market sooner especially in rising markets

✅ Can be removed after building equity

✅ Offers flexibility for first-time and move-up buyers

Cons

❌ Increases your monthly mortgage cost

❌ Doesn’t benefit you directly it protects the lender

❌ Can be expensive over time if not removed

❌ May be hard to remove without appreciation or extra payments

Real Example: PMI in Charlotte, NC

Let’s say you're buying a $375,000 home in Charlotte, NC with 5% down ($18,750). You borrow $356,250.

If your PMI rate is 0.75%, your annual PMI is about $2,671 or $222/month.

By building equity and watching home values, you could remove PMI within 3–5 years.

This is why understanding what PMI is isn’t just helpful it’s strategic. You’ll know how to budget, plan for equity milestones, and eventually lower your monthly payments.

Final Thoughts: Should You Worry About PMI?

Here’s the truth: PMI isn’t a bad thing. In fact, it’s often a useful tool. It helps people get into homes sooner, especially when saving 20% down isn't realistic.

Yes, it adds a cost but it also gives you access to the market.

The key is to:

- Understand what PMI is

- Know your removal options

- Monitor your home equity growth

- Work with a lender and agent who explain your numbers clearly

Ready to Take the Next Step?

If you're house hunting in Charlotte or surrounding areas, I can help break down PMI, loan options, and what makes the most sense for your situation.

I'm Angelina Balatsky with eXp Realty, helping buyers and sellers all over Charlotte, Matthews, Ballantyne, Monroe, and beyond. Let’s get you into your dream home with or without PMI.